This version of the Defined Contribution 2010 Pension Plan has now closed to new entrants and future regular contributions from your employer payroll, following the transfer to Aegon's TargetPlan platform. You can continue to make contributions to the Defined Contribution 2010 Pension Plan, by completing the plan alteration form.

This page and the fund information provided below is specific to the members of the BP Defined Contribution 2010 Pension Plan.

If you're making regular contributions to TargetPlan, you can find TargetPlan fund information when you log into your account.

It is important to think about how you would like to invest your pension contributions.

Depending on how comfortable you are with choosing your investment funds, there are two main approaches to consider:

Lifestyle - have your funds chosen and changed for you

The ‘Lifestyle’ option chooses and changes your mix of funds for you automatically, based on how close you are to your retirement age.

If you invest in the Lifestyle fund, please contact us to let us know at what age you plan to retire so we can begin the process of moving your investments at the right time. We’ll always assume that you plan to retire at age 65, unless you tell us otherwise.

Self-select - choose your own mix from the fund range

The ‘self-select’ option lets you choose a mix of funds from the range of eight different funds covering shares (equities), bonds and cash.

If you do choose self-select funds in place of the Lifestyle fund, you’re taking control of the investment strategy. This means it will be up to you to manage the change from higher-risk, higher-return assets to lower-risk assets in the approach to retirement.

Self-select in combination with the Lifestyle option

You can also choose to put some of your pension contribution in self-select and some in the Lifestyle option.

This might be something you’d consider if you like the switching approach of Lifestyle, but aren’t comfortable with the potential volatility from one year to the next of having all of your assets invested (through Lifestyle) in shares up until 10 years before retirement. In this case, a combination of the Lifestyle fund and one of the Self-select bond funds might be worth thinking about.

Before you decide which option suits you best, read on for more information about the Self-select option, followed by the Lifestyle option.

The value of an investment can fall as well as rise for a number of reasons, for example market and currency movements. You could get back less than you invest.

More about the Lifestyle fund

This fund has a two stage investment approach aimed at investors who want to try to protect their savings from undue volatility as they approach retirement and prefer not to manage this process themselves.

In the first stage, the Accumulation Stage, your contributions are invested in the DCP Global Equities fund which invests in a mix of equities (shares) from around the world with the aim of growing your savings.

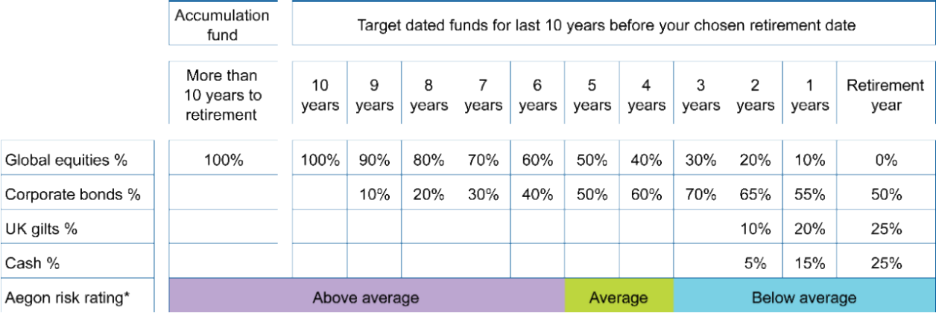

The second stage, the De-risking Stage, starts when you're 10 years from retirement and aims to reduce the risk your savings are exposed to. At this point, we move your existing savings and future contributions into the Target Dated lifestyle fund for your retirement year. This fund gradually and progressively moves your investment from equities into lower risk investments such as bonds and cash. This process happens automatically.

Stage 1 — building up your savings in your younger years

In stage 1 when you are still building up your savings (the ‘accumulation’ stage), your contributions into the Lifestyle fund are invested in the DCP Global Equities fund. This fund has a two stage investment approach aimed at investors who want to protect their savings from undue volatility as they approach retirement and prefer not to manage this process themselves.

Please note the fund names in any communications from us will show the prefix 'DCP' (which stands for Defined Contribution Plan).

Stage 2 — preserving your savings as you near retirement

Ten years from retirement, the amount that you’ve invested in the Lifestyle fund is moved into a Target Dated fund that matches your planned retirement year. Your future contributions will also be paid into that fund. For example, if you’re 55 in 2020 and you’ve chosen 65 as your retirement age, your Target Dated fund will be the 2030 fund.

We will change the asset mix of the Target Dated fund to move in gradual steps from 100% global shares (equities) into UK corporate bonds, UK gilts and cash. This process is designed to help preserve the size of pension you can buy with your fund at retirement. It happens automatically, so you won’t need to do anything to start this change.

During this stage the name of your fund will change to reflect your retirement year. For example, if you intend to retire in 2029, your fund name will change to DCP Lifestyle fund (2029).

There are different factsheets for our Lifestyle fund depending on whether you're invested in the main fund or have started to move into funds that aim to suit your needs as you near retirement. These are the fund factsheets relating to the Lifestyle fund when you're 10 years or less from retirement.

| Target retirement year | Investment fund |

|---|---|

| 2036 | DCP Lifestyle fund (2036) |

| 2035 | DCP Lifestyle fund (2035) |

| 2034 | DCP Lifestyle fund (2034) |

| 2033 | DCP Lifestyle fund (2033) |

| 2032 | DCP Lifestyle fund (2032) |

| 2031 | DCP Lifestyle fund (2031) |

| 2030 | DCP Lifestyle fund (2030) |

| 2029 | DCP Lifestyle fund (2029) |

| 2028 | DCP Lifestyle fund (2028) |

| 2027 | DCP Lifestyle fund (2027) |

| 2026 | DCP Lifestyle fund (2026) |

The following table shows:

- How the fund’s asset mix changes in the last 10 years before retirement

- How the risk rating of the fund falls from above average at first, to below average in the retirement year.

* We grade each fund in relation to its risk against all other funds in our insured range. The rating is not an industry standard and it has no relevance or relationship to the fund risk ratings of other fund providers.

Each fund progressively changes its asset mix each month. It makes these changes through 12 equal steps throughout each calendar year until it reaches the target asset mix at the start of the following year.

We use long-dated corporate bonds and gilts (UK government bonds) and long gilts in Stage 2 of the Lifestyle investment process because of their inverse relationship to annuity rates. Broadly, this means that when annuity rates (which tell you how much annuity you will get per year) go down, the value of a pension fund that's invested in long gilts or corporate bonds is likely to go up, and the other way around.

This means that if you invest in long gilts or corporate bonds, the level of income you get at retirement is less likely to change dramatically if annuity rates move up or down just before you retire. But you should be aware that the value of bonds and long gilts can go down as well as up - just like any other asset that can be traded - although the movements won’t normally be as large as those associated with shares (equities).

Please note this relationship is not perfect and there are other factors that can affect the value of bonds, long gilts and annuity rates.

Retirement phase

If your target retirement year has passed, but you haven't yet moved you'll be moved automatically into the DCP Retirement fund.

This fund is for members of the BP DCP scheme invested in a DCP Retirement Year fund, who have reached their selected retirement date (SRD) and have not yet bought an annuity. These members will automatically be switched into this fund at their SRD. It's specifically designed as a temporary, short-term holding fund that aims to help preserve the amount of pension investors can buy through an annuity. It does so by investing 50% in long-dated corporate bonds (maturities of 15 years or more) through the DCP GBP Corporate Bonds fund and 25% in long-dated UK government bonds (gilts with maturities of 15 years or more) through the passively managed DCP UK Gilts fund. These funds aim to lessen the effects that fluctuating interest rates have on annuity rates so that scheme members in the fund don't suffer a dramatic drop in their potential pension income when they buy an annuity. The fund also invests 25% in the DCP Cash fund, in order to provide for investors' tax-free cash allowance.

As part of the governance framework, the fund’s performance will be monitored against the underlying funds’ benchmarks.

Aegon risk rating

As retirement approaches, most people will want to try to preserve their retirement savings from market volatility. You may be comfortable managing this yourself or you can leave it to us by investing in the Lifestyle fund.

The DCP Lifestyle fund starts off investing in Above-average risk investments which gradually changes in the 10 years before your retirement year to invest in more Below-average risk investments.

From time to time we’ll review the structure of the Lifestyle fund to make sure it's suitable for the existing economic conditions. We might make changes if we need to. You’ll find more detail about this in your policy conditions documents.

Take a look at our FAQ for more information about our risk ratings.

More about self-select funds

The funds available include the building blocks that we use to construct the Lifestyle fund — DCP Global Equities fund, the DCP GBP Corporate Bonds fund, the DCP UK Gilts fund and the DCP Cash fund.

You can click on the fund names to download a factsheet with more information.

Please note the fund names in any communications from us will show the prefix ‘DCP’ (which stands for Defined Contribution Plan). This will include yearly statements and any online services such as fund switching. So, for example, the UK Gilts fund will be shown as the DCP UK Gilts fund.

The DCP Global Equities fund aims to achieve long-term capital growth by investing in a broad range of shares of companies from across the world over a large number of industry sectors. It is constructed by investing in the equity funds within the DCP fund range. It currently invests 30% in UK equities, 60% in overseas equities and 10% in emerging markets equities but this can vary slightly as market values change. The manager may also decide to change it to ensure it remains consistent with the fund's aim.

This fund is also one of the current building blocks used for the Lifestyle fund.

Current benchmark

The DCP Global Equities fund's performance is monitored against a composite benchmark made up of the three funds detailed above (comprising 60% FTSE Developed ex-UK Custom ESG Screened Index, 30% FTSE All Share Custom ESG Screened Index and 10% FTSE Emerging Markets).

Aegon risk rating

Above average

The DCP UK Equities fund aims to achieve long-term capital growth by investing in the shares of companies listed on the London Stock Exchange. It is passively managed, which means it aims to perform broadly in line with its benchmark (FTSE All Share Custom ESG Screened Index) by largely investing in the same companies and in the same proportions. By doing so, it allows exposure to a broad range of companies over a number of industry sectors.

This fund is one of the building blocks of the Global Equities fund.

Current benchmark

DC UK Eq BM

Aegon risk rating

Above average

The DCP Overseas Equities fund aims to achieve long-term capital growth by investing in the shares of companies listed on the overseas stock exchanges of developed stock markets. It is passively managed, which means it aims to perform broadly in line with its benchmark (FTSE Developed ex-UK Custom ESG Screened Index) by largely investing in the same companies and in the same proportions. By doing so, it allows exposure to a very broad range of companies over a large number of industry sectors. The fund's investments will be made directly into constituent companies and via other transferable securities giving exposure to such companies.

This fund is one of the building blocks of the Global Equities fund.

Current benchmark

DCP Overseas Eq BM

Aegon risk rating

Above average

The DCP Emerging Markets Equities fund aims to achieve long-term capital growth by investing in the shares of companies listed on emerging market stock exchanges. It is passively managed, which means it aims to perform broadly in line with its benchmark by largely investing in the same companies and in the same proportions. By doing so, it allows exposure to a very broad range of companies over a large number of industry sectors. The fund's investments will be made directly into constituent companies and via other transferable securities giving exposure to such companies. The fund may also invest in permitted money market instruments, permitted deposits, and units in collective investment schemes. Derivatives and forward transactions may be used for the purposes of efficient portfolio management.

This fund is one of the building blocks of the Global Equities fund.

Current benchmark

FTSE Emerging

Aegon risk rating

Higher

The DCP UK Gilts fund aims to achieve capital growth by investing in sterling denominated UK government fixed interest bonds (gilts). It is passively managed, which means it aims to perform broadly in line with its benchmark by largely investing in the same bonds and in the same proportions. Investing in UK gilts, backed by the UK government, carries little risk of default, however this low level of risk is reflected in the rate of interest earned. The fixed rate of interest attached to these investments does not offer explicit protection against changes in price inflation.

This fund is also one of the current building blocks used for the Lifestyle fund.

Current benchmark

FTSE Actuaries UK Conventional Gilts over 15 Years Index

Aegon risk rating

Below average

The DCP GBP Corporate Bonds fund aims to achieve capital growth and income by predominantly investing in a wide range of Sterling denominated investment grade corporate bonds with maturities of 15 years or greater. It is passively managed, which means it aims to perform broadly in line with its benchmark [which is the Markit iBoxx Sterling Non-Gilts Over 15 Years Index] by largely investing in the bonds which constitute this index. Investing in corporate bonds will typically carry more risk compared to government bonds due to the risk of a company defaulting. Generally, bonds with a longer maturity will typically be more sensitive to interest rate changes than those with shorter maturities.

This fund is also one of the current building blocks used for the Lifestyle fund.

Current benchmark

Markit iBoxx Sterling Non-Gilts Over 15 Years Index

Aegon risk rating

Below average

The DCP UK Index-Linked Bonds fund aims to achieve capital growth by investing in index-linked sterling denominated bonds. It may invest in UK government-issued or in non-government index-linked bonds. It is passively managed, which means it aims to perform broadly in line with its benchmark by largely investing in the same bonds and in the same proportions. The returns from index-linked bonds are linked to the Retail Prices Index (RPI), which measures inflation in the UK, and are intended to offer protection against UK inflation.

Current benchmark

FTSE Actuaries UK Index-Linked Gilts Over 5 Years Index

Aegon risk rating

Below average

The DCP Cash fund aims to achieve an investment return that is in line with wholesale money market short-term interest rates (in general, wholesale rates are higher than retail rates). Specifically, the fund seeks to better the return of its benchmark, the Sterling Overnight Index Average (SONIA). It invests in a diversified portfolio of high quality (those with a minimum credit rating of A1 or equivalent) money market instruments.

This fund is also one of the current building blocks used for the Lifestyle fund.

Current benchmark

Bank of England Sterling Overnight Index Average

Aegon risk rating

Minimal

How BP chose the fund range

BP made sure that all of these funds were:

- Passive funds – these funds aim to follow the returns of an external market index (for example the FTSE All-Share Index)1.

- Transparent - You can see what the underlying fund has invested in and you can see how close the fund is to meeting its benchmark.

- Lower cost - because the cost to the investment manager of running a passive fund is lower than an actively managed fund.

- Highly diversified - each fund invests across a wide range of underlying investments, and the fund range as a whole provides you with access to most types of asset classes.

1 Remember that the effects of annual management charges and differences in the timing of pricing between the index and the fund mean their performance will never be exactly the same.

Please note there’s no guarantee that the funds will achieve what they aim to. We don't guarantee benefits and the value of investments can go down as well as up. For advice as to whether a fund is suitable for you, please speak to a financial adviser. If you don’t have a financial adviser, you can visit MoneyHelper to find the right one for you.

While there’s no guarantee that the investment manager will meet the performance of the fund benchmarks, we do monitor these funds through a strict governance process. You can be confident that these funds are given the highest scrutiny. But governance is not just about making sure that a fund’s performance is in line with its objectives - it’s also about quality control. This means there may be changes to the fund range in the future as we keep making sure that the funds we offer continue to meet expectations.

Please note that the links below this line don’t apply to the DC2010 plan – these are links to generic Aegon information.