Aegon LifePath funds are default investment options for TargetPlan and the Aegon Master Trust. If you don’t choose how your pension savings are invested, they may automatically be placed into one of these funds, based on the fund your scheme has chosen as its default.

These funds are designed to make investing straightforward by managing your pension investments for you. Our experts adjust them over time as your needs change, supporting you from day one through to retirement.

To see where your pension is currently invested, log in to your TargetPlan account and select ‘View and manage’.

How Aegon LifePath funds work

The Aegon LifePath funds are target dated funds, meaning they automatically adjust what they invest in as you get closer to retirement. Early on, they invest in assets designed to grow your savings. As retirement approaches, they shift to invest in assets which are typically considered to be lower-risk, aiming to preserve the savings you’ve built up. These funds invest across a mix of assets, like equities and bonds and in different world regions. This approach, called diversification, helps spread risk by not putting all your eggs in one basket.

If you invest in Aegon LifePath, you’ll be put into a fund version that is managed in line with the year you plan to retire and it will include the year in the fund name. For example, if you plan to retire in 2035, you’ll be put into a fund that has 2034 – 2036 in its name.

Grow

In your early working years, the fund focuses on growing your pension savings. Your money is mainly invested in equities (company shares), which carry more risk but typically offer greater potential for long-term growth.

Preserve

As you get closer to retirement, the fund gradually and automatically moves into investments designed to prepare your savings for retirement, such as bonds. How this works will depend on which Aegon LifePath fund you're invested in. This process aims to help preserve the retirement income you'll be able to take and starts 15 years before your chosen retirement age.

Access

What happens to your savings once you’ve reached your target retirement age will depend on the specific Aegon LifePath fund you’re invested in.

The value of investments may go down as well as up and you may get back less than you invested. Please see fund factsheets for full details, including fund-specific risks. If you're unsure about how to invest, please speak to a financial adviser.

We're making changes to the investment mix for Aegon LifePath funds from summer 2026. Find out more in our fund update.

Where Aegon LifePath funds invest

There are three Aegon LifePath funds to choose from - Flexi, Retirement, and Capital. They all follow the same investment approach, but are designed to support different ways of accessing your pension when you retire.

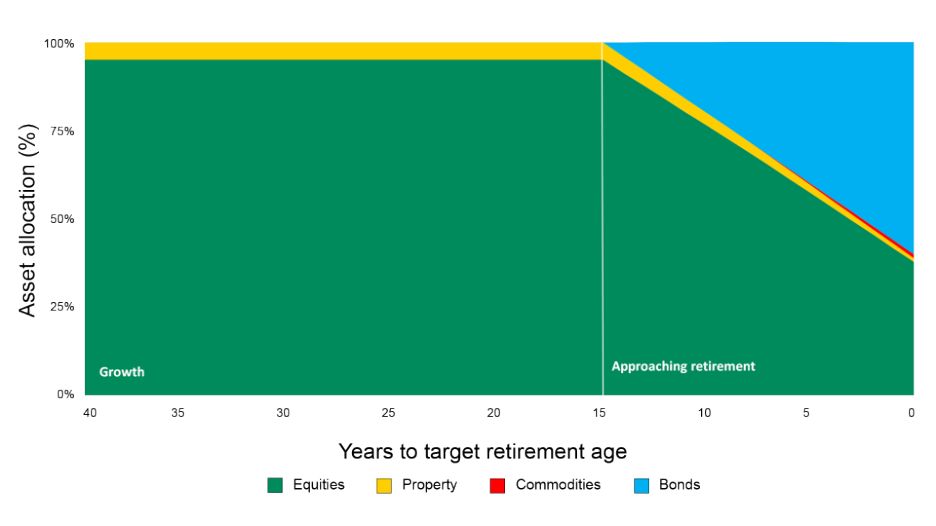

Aegon LifePath Flexi is designed for people who plan to stay invested in retirement and take a flexible income (drawdown).

- Fully invested in growth assets in early years

- From 15 years before retirement, gradually shifts to investments that are considered to be less risky

- At target retirement age: Approximately 40% equities (shares in companies) / 60% fixed income (loans to governments or companies)

This fund assumes you’ll remain invested and draw an income, so values can fall as well as rise, and income isn’t guaranteed. You could run out of money, and moving to lower-risk assets may limit growth.

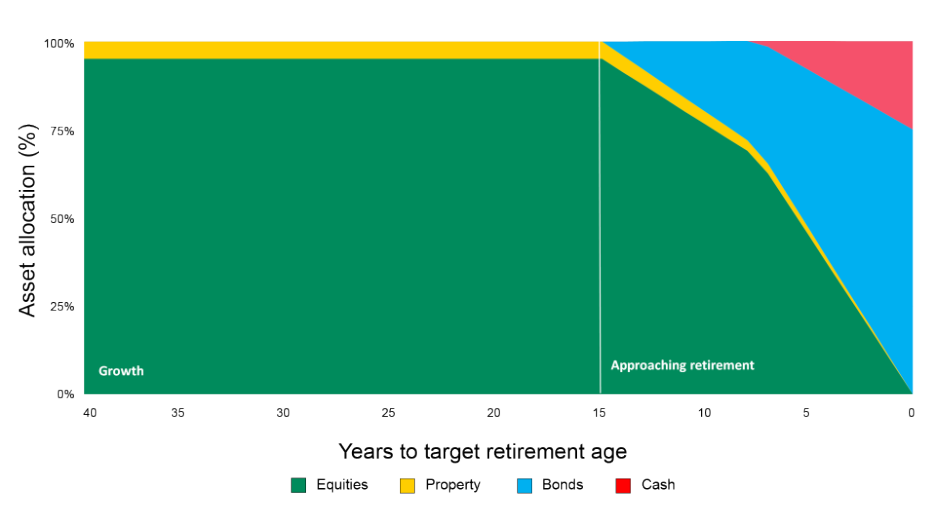

Aegon LifePath Retirement is designed for people planning to convert their savings into a guaranteed income by buying an annuity.

- Fully invested in growth assets in early years

- From 15 years before retirement, gradually shifts to investments that are designed to preserve the size of annuity you can buy on retirement, although this isn't guaranteed.

- 25% is also moved into cash, to cater for your tax free entitlement on retirement (based on our understanding of current taxation law and HMRC practice, which may change).

- At target retirement age: Approximately 75% fixed income / 25% cash

Not intended for long-term investing once your reach target retirement age. This fund is unlikely to be suitable for those who don't plan to buy an annuity on retirement. The value of your savings can fall as well as rise and the move into different investments may limit growth potential.

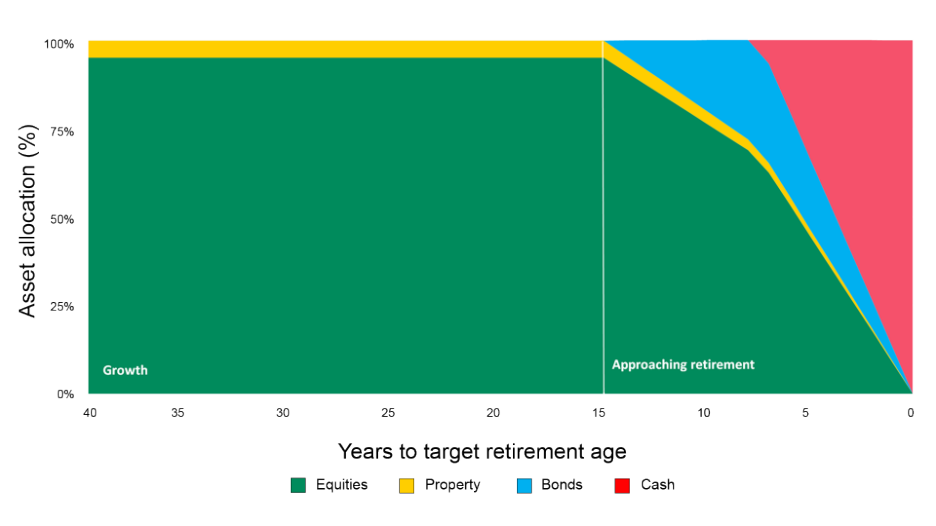

Aegon LifePath Capital is designed for people who plan to take their pension as a cash lump sum at retirement.

- Fully invested in growth assets in early years

- From 15 years before retirement, gradually shifts to investments that are considered to be lower-risk, and then into cash

- At target retirement age: 100% cash

Not intended for investing once your reach target retirement age as returns are unlikely to keep pace with inflation. The value of your savings can fall as well as rise. Moving into less risky assets will limit this fund's growth potential.

* Private markets are investments made directly into businesses or projects that aren't bought or sold on public markets.