At Aegon, helping our customers improve their financial wellbeing is at our heart. And we know financial advisers like you, play a key role in this journey for your clients.

So, to better understand people’s relationship with money, our Centre for Behavioural Research conducted extensive research asking 10,021 UK residents a series of questions. This was a follow up to our flagship research the year before. It gave us a really robust understanding of how financially well the UK is, the ability to draw conclusions and a clear view of where the opportunities are for improvement. The study was nationally representative in terms of location, age and gender.

What does financial wellbeing mean?

Financial wellbeing isn’t just about your financial position here and now – it’s also about your long-term ability to be financially well. One way to look at financial wellbeing is to concentrate on two things:

- Having security around money – now and in the future.

- Knowing what makes us happy and having money goals to achieve that happiness.

Our analysis found a mental focus on what makes us feel happy (joy) and useful (purpose) plus a plan to achieve that now and in the future, was a much stronger indicator for financial wellbeing than overall wealth.

And part of finding joy and purpose – or defining them – is to help your clients to fully understand how they think about money and their financial resilience.

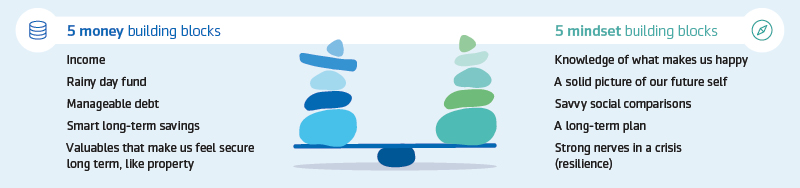

The ten financial wellbeing building blocks

Our research revealed that the key to building financial wellbeing is to have money building blocks and mindset building blocks.

| 5 money building blocks | 5 mindset building blocks |

|---|---|

| income | Knowledge of what makes us happy |

| Raint day fund | A solid picture of our future self |

| Manageable debt | Savvy social comparisions |

| Smart long-term savings | A long-term plan |

| Valuables that make us feel secure long term, like property | Strong nerves in a crisis (resilience) |

But it’s also about balance. Even if your clients have their money building blocks nailed, they won’t achieve optimal levels of financial wellbeing without a well-considered and focused mindset too.

What was clear from our research was that mindset scores were lower than money scores, and the scores did not improve much the higher peoples’ incomes were.

Find out what our research tells us about each building block

The UK’s financial wellbeing score

Our research gave us a really interesting insight into the UK landscape and we wanted to quantify our findings into something more concrete. Out of this our Financial Wellbeing Index was created.

What we found could change the way clients look at money, for the better. People with the best financial wellbeing scores did well in both money and mindset blocks.

'The best possible combination is to be what we call the 'all-rounder'.'

All money and no long-term plan for happiness was no better overall for financial wellbeing

than no money and all plan. On average, people in the UK fall somewhere in the middle of having good money and good mindset building blocks.

So what is an ‘all-rounder’?

All-rounders are very financial comfortable and can enjoy life now whilst planning for the future. They balance the importance of money and mindset well and are ready for what the future holds.

But only 18% of people are here already.

How to help your clients be an ‘all-rounder’

Recognising where your clients are on this scale could help identify ways to help them. Improving the UK’s financial wellbeing means working together on the essentials:

- Ask them to focus on how/why they spend – do they spend to satisfy a need? Are there cheaper ways to satisfy the same need? This isn’t about asking them to justify what they spend their money on but to draw more focus on money in and money out as it might help them to rebalance the scale.

- Teach your clients how to think long-term – this plays a big part in achieving financial wellbeing. Experts have calculated people need to put away closer to 15% a month (including employer contributions).1

- Ask them to describe their joy and purpose – things your clients do to relax (joy) and things they do to feel competent, engaged or useful (purpose). Tuning into this can also help them focus on how/why they spend money.

- Encourage them to think about their future self – who are they, where are they, what does their future look and feel like. If you can’t see or feel it too, it’s not concrete enough.

Tools to support you

Our in-depth digital flipbook explores our research even further and provides clients with recommendations to help them think and act positively about their future - going deeper than budgeting tools and savings rules an shows how financial wellbeing is possible for everyone.

We’ve also created our summary of our insight into the nation’s financial wellbeing – just for advisers and employers.

Plus our financial wellbeing tool and Picture your best life tool can help your clients identify areas of their financial wellbeing you can work on together.

Find out more about financial wellbeing at aegon.co.uk/financialwellbeing.

- Independent Review of Retirement Income: We Need a National Narrative: Building a Consensus around Retirement Income, page 62. Data source, Pensions Institute, David Blake, March 2016.